Written by Jan Aengenvoort, Next Kraftwerke

Welcome back to the second part of Zondits’ exploration of virtual power plants! Part 1 of the series provided a brief introduction to VPPs. In part 2, we answer the following question:

What is the Business Model of a VPP?

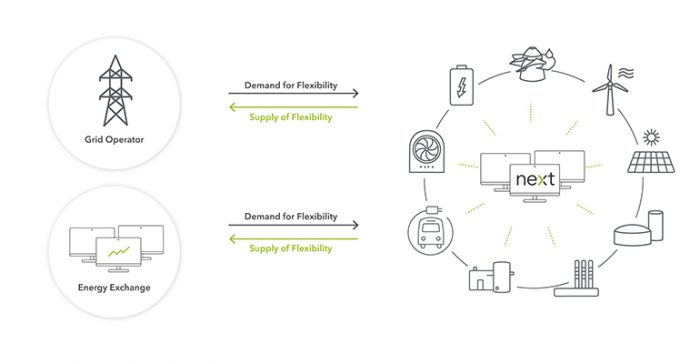

For a couple of years now, the role of the virtual power plant (VPP) has been establishing itself in the energy industry. Today, it is pretty clear what a VPP is and why it makes sense to network, forecast, optimize, and dispatch a fleet of coordinated distributed energy resources (DER) such as wind, solar, bioenergy, hydropower, batteries, electrolyzers, and many more. But how do you make money with a VPP? What’s the business case of a VPP operator/aggregator?

Forecasting, Trading, and Curtailment of Renewable Energy

As the share of renewables rises in many energy markets around the world, the question of how to manage the infeed of those very resources arises more sharply. While the percentage of renewables in the grid may be low (and subsequently low in the portfolio of power traders) and the volatility of renewables may not pose a big challenge in the beginning, there seems to be a certain threshold after which it becomes a financial burden for the portfolio manager not to forecast and dispatch renewables as accurately as possible.

Let’s take your generic utility as an

example. In the 2000s and the early 2010s, the utility may only have had a

couple of megawatts of solar and wind in its larger portfolio, so the

intermittency of PV and wind infeed didn’t have a big effect on its overall

generation – their fluctuations were basically muted by the general baseline of

conventional power production. But as soon as that utility ramped up its

renewable generation to, let’s say, 20% of its portfolio, solar and wind have a

larger effect on the everyday management of the utility’s overall portfolio.

Forecasts suddenly turn out to be wrong. Wind and solar are not curtailed if

prices on spot markets turn negative and, so, instead of making money, they

cost money. Nominations of expected infeed to the Balancing Authority (e.g.,

Transmission System Operators) have huge deltas. Trading limps behind and is

punished by expensive balancing costs for ex post portfolio corrections. Why

does this happen? Because by nature, it’s more difficult to project the

trajectory of PV or wind power infeed than that of a baseline conventional

power plant. For one, there may not be the same historical data to rely on yet.

And in many cases, the utility doesn’t even know what its renewable portfolio

is currently producing.

So the utility turns to the technology of a virtual power plant to get a grasp

on things. By doing this, all renewable energy sources (RES) in the portfolio

of that utility are networked through remote control units, so that the

aggregated volume of power generation from all distributed plants is displayed

live, and all or individual PV and wind farms can be curtailed from the trading

floor. Furthermore, historic data is either added to the system from

DSO-metered data or it starts building itself once all plants are sending their

infeed. Now you add some meteorological forecast data and put it all through

statistical analysis and machine-learning algorithms to gain the best possible

forecast of the entire renewable portfolio.

Where is the money in that, you may ask? Four sources:

- First, the portfolio manager saves balancing costs that incur in many energy markets around the world when the forecasts of a power trader’s portfolio don’t meet the actual feed-in.

- The portfolio manager or the trader can now curtail the RES portfolio as soon as prices fall below zero.

- In case the RES portfolio contains some sort of bioenergy or hydropower – or other dispatchable renewable energies like geothermal, etc. – the trader may use the VPP to optimize and steer the generation schedule of those assets, e.g., by ramping them up when power prices are projected to go up. This way, he is now able to beat average prices on short-term markets and share the additional revenues with the plant operator.

Lastly, by understanding their own RES portfolio better, the trader also learns more about the whole market situation and where spot market prices will be heading, since PV and wind infeed tend to become the price drivers in energy markets with higher shares of renewables. The trader then uses that information to take up not only a safer standing but also a potentially more lucrative trading position.

Table A. VPP Business Case: “Forecasting, Trading, and Curtailment of Renewable Energy”

Aggregation of Grid Flexibility from Renewable Energy

Table A shows how a VPP helps with the management of a RES portfolio from a trader’s perspective. But what about the actual physical fluctuations, especially now that the trader knows more about them and earlier but which nevertheless occur and need to be physically balanced within the grid? First of all, more lead time due to improved forecasts already enables the entire market (other traders and dispatchers) to react more quickly to fluctuations and thus to counter them before they cause pain in the system. But more importantly, a VPP not only networks renewables to improve forecasting but also to provide ancillary services to the grid operator. After receiving a signal to ramp up or down power generation from the grid operator, the central control system of the VPP splits up that signal to hundreds or thousands of individual signals for the individual dispatchable renewable power plants, taking into account their restrictions on response time, filling levels, heat generation, you name it. It then automatically sends the ramping signal to the involved networked units and ramps them up or down to support the grid frequency and to counter the very same fluctuations that other units in the VPP – mostly PV and wind – have caused in the first place.

Again, where’s the money? Since short-term reserves are extremely important to run the electricity system and to provide the security of supply that we all enjoy every day, these reserves have a significant price tag. Tapping into that potential by providing short-term reserves to the grid operator is an excellent business case for aggregators, especially because they don’t need to invest in the physical buildup of flexible power generation (e.g., gas-fired power plants or pumped hydro storage) but merely in the networking of existing smaller-scale flexible units. Traditionally, the VPP operator splits the revenues from successful capacity tenders and actual deliveries of ancillary services with the operators of the dispatchable RES unit that is networked in the VPP. In non-liberalized markets where tenders for these reserves don’t exist yet, the Transmission System Operator (TSO) can run the VPP by himself to harvest the flexibility from distributed energy resources.

Table B. VPP Business Case: “Aggregation of Grid Flexibility from Renewable Energy”

Demand Response Aggregator

Basically a subset of Table B, an aggregator might opt to not only aggregate power generating units but also (or exclusively) demand side units to provide ancillary services to the grid. The power grid doesn’t care if you ramp up the power generation of a hydropower plant or if you ramp down the power consumption of, let’s say, an air conditioner or the cooling system of a warehouse. The effect on the grid frequency is the same, so there is also a business case for aggregators (the term “virtual power plant” doesn’t seem to apply here) on the demand side. In some energy markets, there are even special tender schemes for reserves (on top of the ancillary services markets) that are supplied by the demand side in order to promote their development. While the implementation of demand response aggregation is a very regional phenomenon today (US, Australia) and often limited to commercial and industrial power consumers, it holds gigantic potential once tiny flexibilities on the household level (e.g., EV batteries, heating pumps, AC units) are aggregated and become more active on the energy market.

Moreover, a fleet of aggregated demand response units may also be used to not only deliver ancillary services to TSOs but also to dispatch consumption of the networked units to times of low prices on spot markets – lowering the costs for power procurement for each asset with a share for the VPP operator. Thanks to the automated consideration of each unit’s individual restrictions, these time-of-use tariffs may differ from unit to unit.

Table C. VPP Business Case: “Demand Response Aggregator”

Final Thoughts

Like every typology, this one also has its flaws. The boundaries between the different business cases are fluid, of course, depending on the structure and regulation of the energy market where the aggregator is active, but also depending on current and ever-changing price signals in these markets. You can also easily imagine – and find – aggregators that combine all three business cases in one VPP. But one thing is for sure: the large-scale integration of renewables into grids and markets needs a systematic and well-coordinated approach through VPPs – and there is money to be made with it.

If you want to learn more about various business models of VPPs and how they fit in the regulatory frameworks of unbounded and vertically integrated energy markets, join the webinars organised by Next Kraftwerke. More information under: https://www.next-kraftwerke.com/company/webinars